As the owner of credit repair software, I’ve encountered numerous consumers who have fallen victim to credit repair scams. Many came to me frustrated and bewildered. They have been promised quick fixes to their credit woes, only to find themselves deeper in financial turmoil.

To help you out, let me shed light on the insidious nature of credit repair fraud. Its impact on consumers, detection methods, regulatory responses against these schemes, common tactics used by credit repair frauds, prevention strategies, and the role of credit repair software in combating this menace.

First, let’s understand the real meaning of credit repair fraud if you haven’t heard of it yet.

What is Credit Repair Fraud?

Credit repair fraud encompasses deceptive practices aimed at manipulating credit reports to improve creditworthiness unlawfully. Fraudulent individuals may promise to improve your creditworthiness quickly, often for an upfront fee that is against the law.

Moreover, they exploit loopholes in credit reporting systems. For instance, they falsify information, dispute accurate negative items on credit reports, or misrepresent their ability to remove negative marks. These schemes often involve illegal activities such as identity theft, false documentation, and misleading advertising. They target individuals desperate to improve their credit standing.

The Impact of Credit Repair Fraud on Consumers

Credit repair fraud can have devastating consequences on you as a consumer. Firstly, it can result in financial losses. You may end up paying fees for services that fail to deliver the promised results.

Moreover, fraudulent activities, such as disputing accurate negative items on your credit report, can worsen your credit situation. Instead of improving it. This can lead to higher interest rates on loans and credit cards, making it more expensive for you to borrow money.

Additionally, if you unknowingly participate in fraudulent actions orchestrated by credit repair scammers, you could face legal consequences and damage to your reputation.

Beyond the financial aspect, being deceived emotionally takes a toll. Dealing with the aftermath of credit repair fraud brings stress. This stress can affect your overall well-being. It can also disturb your peace of mind.

With all these negative impacts, you might be thinking if it’s worthwhile to hired credit repair services? My answer is YES but it’s crucial to know how to avoid them.

How to Detect Fake Credit Repair Companies?

Detecting credit repair fraud requires vigilance and awareness of red flags.

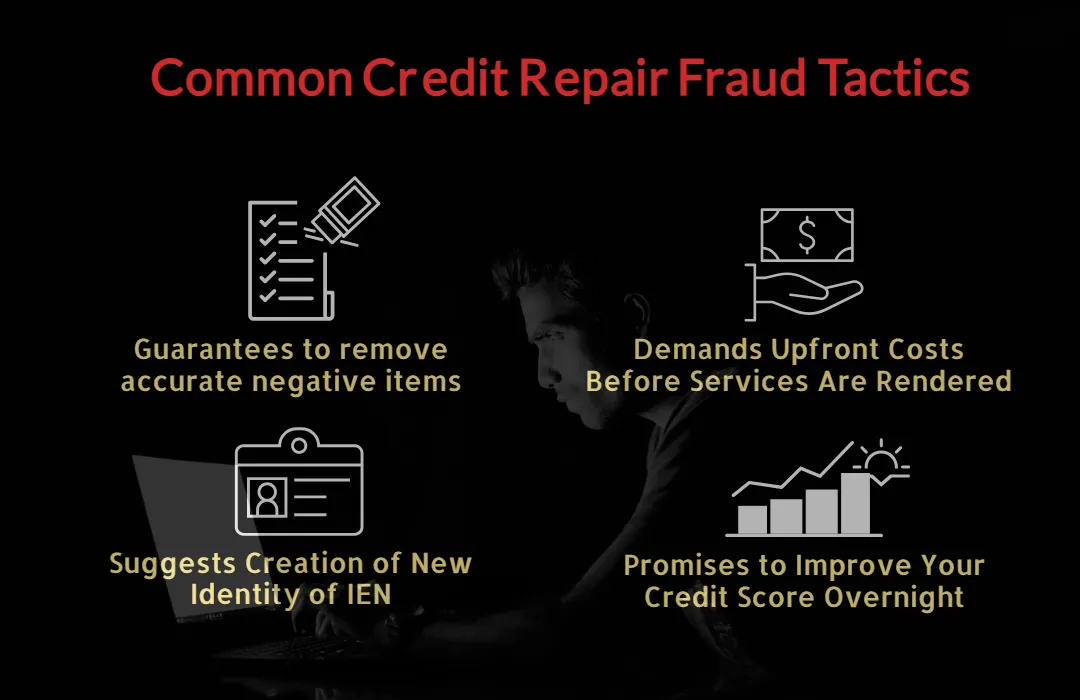

Firstly, be wary of any company or individual that guarantees to remove accurate negative information from your credit report. Or promises to improve your credit score overnight. Such claims are often too good to be true and impossible to achieve. Moreover, it is against Federal credit repair laws to remove accurate information from your credit reports.

Additionally, watch out for high-pressure sales tactics or demands for upfront payment before any services are rendered. Legitimate credit repair companies typically offer a free consultation and only charge fees after work completion. This is also stated in federal law.

Furthermore, be cautious of any requests to create a new identity or apply for an Employer Identification Number (EIN) to establish a new credit profile. These tactics are often associated with fraudulent activities like identity theft.

Finally, regularly monitor your credit reports for unauthorized inquiries, unfamiliar accounts, or inaccuracies that could signal fraudulent activity. If something seems suspicious, trust your instincts and proceed cautiously to avoid falling victim to credit repair fraud.

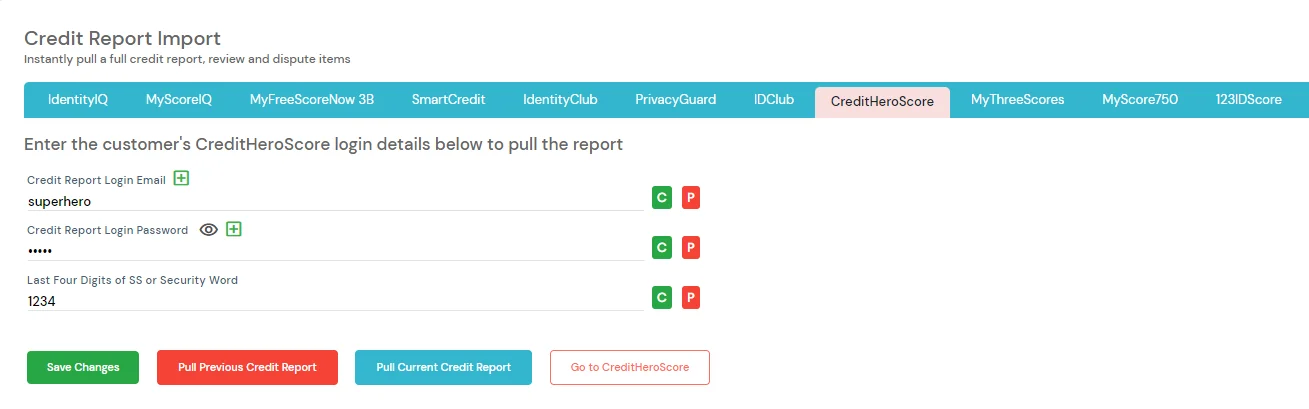

You can use credit repair software with easy access to credit report providers. Credit Money Machine allows you 11 providers to choose from. Identity IQ, My Score IQ, 123ID Score, and Smart Credit, to name a few.

Here’s a screenshot from Credit Money Machine’s Dispute Center. Simply login to your favorite provider to get your lates credit reports.

Your All-in-One Software when it comes to fixing credit.

A great way to identify credit repair scams is to familiarize yourself with the credit repair laws. CROA has a list of requirements for credit repair companies to follow. If your service provider is not following these rules, it is most likely fraud.

Cybersecurity Threats in Credit Fraud:

In the digital age, cybersecurity threats worsen the risk of credit fraud. Cybercriminals employ various tactics to gain unauthorized access to your sensitive financial information. This includes data breaches, phishing scams, malware attacks, and social engineering tactics.

They may infiltrate financial institutions’ systems or compromise your devices to steal login credentials, credit card numbers, and other valuable data. Phishing emails disguised as legitimate communications from banks or credit card companies may trick you into disclosing personal information or clicking on malicious links. Leading to identity theft or fraudulent transactions. Additionally, malware such as keyloggers or ransomware can compromise your devices and capture sensitive information without your knowledge. Putting your finances at risk.

Therefore, it’s essential to stay vigilant. Adopt robust cybersecurity measures, such as using strong passwords, enabling multi-factor authentication, and regularly updating security software. These simple steps help safeguard against cyber threats and protect your financial well-being from credit fraud.

Regulatory Responses to Credit Fraud

Regulatory bodies play a crucial role in combating credit repair companies fraud and holding perpetrators accountable for their actions. These agencies enforce laws and regulations designed to protect consumers from deceptive practices. For example, the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) oversee the enforcement of laws such as the Fair Credit Reporting Act (FCRA) and the Credit Repair Organizations Act (CROA), which prohibit deceptive credit repair practices and require transparency in credit reporting processes.

When credit repair fraud is uncovered, regulatory agencies may take enforcement actions against the perpetrators. They impose fines, restitution requirements, and other penalties to deter future misconduct.

One notable example is the credit repair fraud case of Lexington Law. The Consumer Financial Protection Bureau (CFPB) alleged that the company used deceptive practices by paying third parties to find customers. These affiliates lured potential clients with promises of “rent-to-own homes” and home loans for individuals with bad credit. This is despite having no homes or funds to lend.

Consumers were falsely led to believe that signing up for Lexington Law’s credit repair services would qualify them for a nonexistent home loan in the future. The CFPB also accused Lexington Law employees and executives of potentially aiding these deceptive marketing practices.

The proposed settlement includes a $2.7 billion judgment and over $64 million in civil penalties. The group is also facing a 10-year ban on telemarketing activities. Consequently, Lexington Law filed for Chapter 11 bankruptcy protection, resulting in the loss of 900 jobs and the closure of 80% of its operations.

This case underscores the seriousness with which authorities tackle credit repair fraud. Serving as a warning to wrongdoers and highlighting the crucial role of regulatory oversight in protecting consumers from credit repair company scams.

What To Do If You Have Fallen A Victim Of Such Scheme?

Suppose you are suspecting a credit repair scam. In that case, swift action is essential to minimize potential damages and protect your financial well-being.

Here’s a short video on what to do if you have fallen a victim of credit repair scheme.

Firstly, gather all relevant documentation, including any correspondence, contracts, or statements related to the fraudulent activity.

Next, immediately contact the credit bureaus to report the fraud.

Then, request a freeze or fraud alert on your credit report to prevent further unauthorized activities.

It’s also crucial to notify your bank or credit card issuer if you suspect unauthorized transactions or identity theft.

Additionally, file a complaint with relevant regulatory agencies. You can file a report at CFPB or the Report Fraud at FTC to report the fraud and seek assistance.

Lastly, consider consulting with legal or financial professionals for guidance on proceeding. This may include exploring options for disputing fraudulent charges, recovering lost funds, and repairing any damage to your credit history.

Role of Credit Repair Software in This Menace

Using credit repair software is a smartest way to avoid and detect credit repair fraud. This tool utilizes advanced algorithms and data analytics to monitor your credit reports for any suspicious activities. Or inaccuracies that could signal fraudulent behavior.

Moreover, using credit repair software minimizes your risk of becoming a victim of credit repair company fraud. Utilizing such software eliminates the need to share sensitive information with third parties. Thus reducing the likelihood of data breaches or unauthorized access. For instance, with Credit Money Machine, your sensitive data is securely stored. Hence, ensure that your personal and financial information remains protected.

Furthermore, if you’re operating a credit repair business, the software’s database is exclusively for your use and not shared with other clients. This enhances confidentiality and privacy. Additionally, the software’s portals are devoid of sensitive data that could jeopardize your company’s or clients’ security, mitigating the risk of fraud or data compromise.

With these robust security measures, the credit repair software provides a reliable and secure solution for managing your credit repair needs. At the same time, it safeguards against potential fraudulent activities.

Looking For a Reliable Credit Repair Software for Your Business?

Aside from strict security against data theft, Credit Money Machine is the most complete and fastest credit repair software for businesses. It can process a client in just 15 seconds, which may take an hour for other software. With a single click, the software prepares everything you need to start disputing. It extracts credit reports, identifies errors, and assigns dispute reasons, types, and letters. The only left for you to do is print and mail it to the bureaus. Moreover, it is packed with CRM, Sales, Marketing, Workflow, Invoicing, Emailing, and AI systems to let you manage everything in one interface.

Beginner? Don’t worry, you’ll get live training, a Credit Repair Business Course, and a Winner Strategy when you sign up.

For credit repair business start-ups, I recommend learning about credit repair laws to avoid legal issues and a guide on how to start credit repair business.

Frequently Asked Questions (FAQ) About Credit Repair Fraud

1. What is credit repair fraud, and how does it differ from legitimate credit repair services?

Credit repair fraud involves deceptive practices aimed at manipulating credit reports or scores unlawfully. This often includes false promises to remove accurate negative information from credit reports or misleading consumers into paying fees for ineffective services. Legitimate credit repair services, on the other hand, work within the bounds of the law to help consumers dispute inaccuracies or errors on their credit reports and improve their creditworthiness through legal and ethical means.

2. What are common red flags that may indicate credit repair fraud?

Common red flags include guarantees of specific results or immediate improvements to credit scores, demands for upfront payment before services are rendered, failure to provide a written contract outlining the services offered, and requests to create a new identity or falsify information on credit applications.

3. How can I verify the legitimacy of a credit repair company before using its services?

You can verify the legitimacy of a credit repair company by verifying their credentials and licenses and asking for references from past clients. Moreover, you can research customer reviews and complaints about the company.

4. What are the potential consequences of falling victim to credit repair fraud?

The potential consequences include financial losses from paying fees for ineffective services, further damage to credit scores if fraudulent disputes are made, legal repercussions if involved in illegal activities such as identity theft or false documentation, and emotional distress from being deceived.

5. What steps should I take if I suspect I’ve been a victim of credit repair fraud?

If you suspect you’ve been a victim of credit repair fraud, you should immediately report the incident to credit bureaus and law enforcement agencies. Also, dispute any fraudulent charges or inaccuracies on your credit reports, and consider placing a fraud alert or credit freeze on your accounts. Furthermore, monitor your credit reports regularly for unauthorized activities and seek legal or financial advice for resolving the situation and recovering any losses.