In the world of credit scores, hard inquiries emerge as both a necessity and potential pitfalls. While credit inquiry is an important step in taking out a loan, having too many inquiries can break your credit score. So, many are asking how to remove hard inquiries in 24 hours. Is it possible?

Being in the credit repair industry for over 30 years, let me share my knowledge of credit inquiries, how they affect credit scores, and the steps to remove them.

What is Credit Inquiries?

Before diving into the removal process, it’s essential to understand what credit inquiries are and how they affect credit scores.

Credit inquiries, a.k.a, credit checks or pulls, refer to the instances when a third party requests to view your credit report. These inquiries are typically made by lenders, creditors, or other entities to assess your creditworthiness when you apply for credit. For instance, a credit card, loan, or mortgage.

Types of Credit Inquiries

There are two main types of credit inquiries, and only one can affect your credit scores.

1. Hard Inquiries

These inquiries occur when a potential lender or creditor checks your credit report when you apply for credit. Like a credit card, mortgage, auto loan, or personal loan.

This type of inquiry may lower your score by a few points. Moreover, they stay on your credit report for about 2 years. Fortunately, they can only affect your credit score for the first 12 months.

Furthermore, hard inquiries are visible to creditors and anyone who pulls your credit report. Therefore, it can affect their decision to approve your loan.

2. Soft Inquiries

These inquiries occur where: (1) you check your credit score. (2) when a creditor checks your credit as part of a pre-approved offer. Or (3) when an employer pulls your credit as a background check.

This type of inquiry is considered informational and does not affect credit scores. Moreover, they are only visible on your personal credit report. Therefore, lenders cannot see these inquiries when they review your credit report. Thus, it does not affect their lending decisions and your ability to loan.

In summary, hard inquiries result from your active pursuit of credit and can temporarily impact your credit score. On the other hand, soft inquiries are generally benign and do not affect scores. It’s important to be aware of their differences to know what inquiries to remove.

Steps for Removing Hard Inquiries

Follow these step-by-step guide to effectively remove hard inquiries and potentially improve your credit scores.

Step 1: Obtain Your Credit Reports

Start by obtaining copies of your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion.

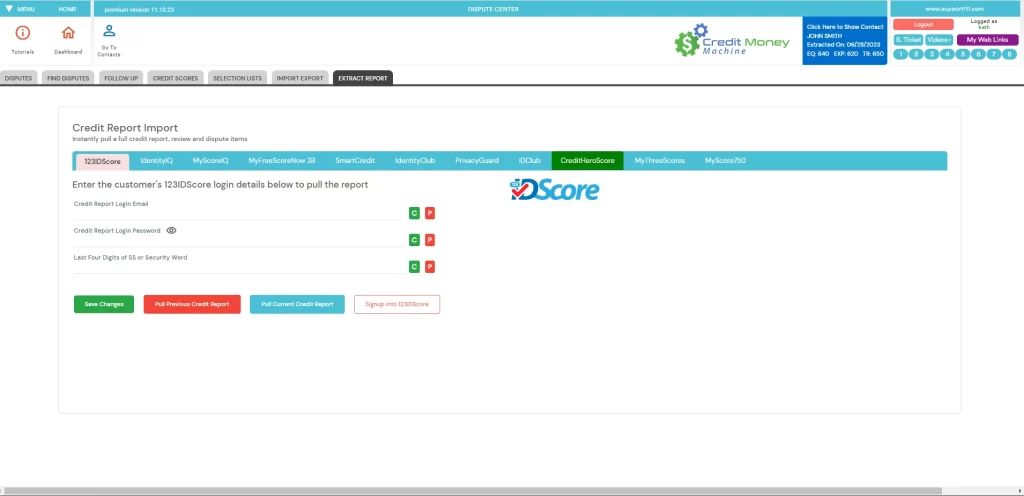

You can get a free credit report from these bureaus on AnnualCreditReport.com every 12 months. You can also get it from other providers like 123IDScore, IdentityIQ, SmartCredit, and CreditHeroScore. You can easily access all these providers and so much more in Credit Money Machine.

Simply go to the Dispute Center, then click the Extract Report button.

Click here to get Credit Money Machine.

Once you have your reports, carefully review them to identify any recent hard inquiries that you believe may be inaccurate or unauthorized.

Here’s a complete guide on how to examine your credit report for discrepancies and negative items. This is for a full credit sweep.

Step 2: Identify Inaccurate Inquiries

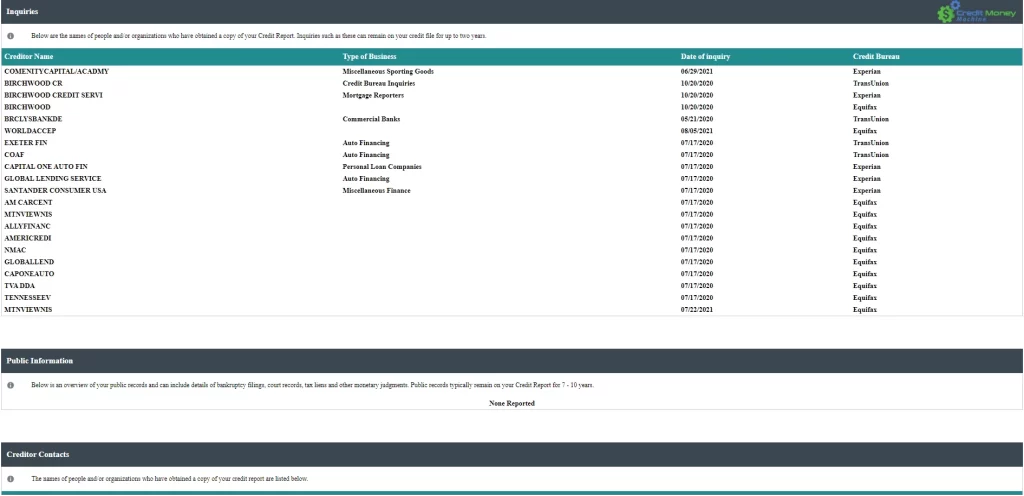

Navigate to the “Inquiries” section in the report. Wherein details such as the creditor’s name, the date, and the purpose of the inquiry are found.

Here is a sample of Inquiries Section in Credit Money Machine interface.

Click here to get Credit Money Machine.

Pay close attention to the information in each inquiry. Remember, hard inquiries are usually associated with credit applications. In contrast, soft inquiries are often for non-credit-related purposes, which do not affect credit scores.

Thoroughly check each hard inquiry for inaccuracies or discrepancies in names, dates, and other details. Look for inquiries that you did not authorize. Or those related to credit applications you did not submit. These are the inquiries that you can remove and help improve your credit scores.

Focus on the recent hard inquiries. Especially within the last 12 months. Since hard inquiries over a year old can no longer affect your credit scores.

Also, look for clustered or multiple hard inquiries within a short period, especially if unrelated to a single credit event.

Multiple Inquiries that Are Considered Single Credit Event

It’s common for individuals to shop around for the best terms when seeking a mortgage or an auto loan. Credit scoring models typically recognize this and treat multiple inquiries for certain types of credit within a short window as a single inquiry. Thus minimizing the impact on your score.

The Impact of Multiple Unrelated Hard Inquiries in A Short Period

Lenders often interpret multiple recent inquiries as a sign that you might be actively seeking additional credit. This indicates financial stress or an increased risk. Therefore, if you find unrelated and discrepancies in the cluster of hard inquiries, they can be removed.

However, if you truly have multiple unrelated credit inquiries in a short timeframe. For instance, inquiring about credit cards, personal loans, student loans, and auto loans in a matter of 3 months without a specific financial goal. Like buying a house or a car. Then, they are deemed to be unrelated and cannot be removed.

Step 3: Dispute Inaccurate Inquiries

After reviewing your credit reports and gathering data to substantiate inaccuracies, the next step is to initiate the dispute process. Begin by contacting the credit bureaus—Equifax, Experian, and TransUnion—that have inaccuracy. You can contact them through their online dispute platforms, mail, or phone.

Clearly outline the discrepancies you’ve identified in the inquiries section of your credit report. Then, provide specific details such as incorrect names, dates, or inquiries tied to accounts you didn’t apply for. Attach any supporting documentation you’ve collected as evidence. This can be emails, letters, or records that contradict the inaccurate information. Be concise and precise in your dispute communication to ensure the credit bureaus can efficiently process your claim.

Simultaneously, it’s crucial to contact the creditors associated with the inaccuracies. Provide them with the same documentation and a detailed explanation of the errors. While the credit bureaus are responsible for updating your credit report, engaging directly with creditors can expedite the correction process.

Furthermore, keep a meticulous record of all communications, including dates and names of individuals spoken to. This documentation may prove invaluable in case of further disputes or follow-up actions.

Patience is key during this process, as credit bureaus typically have 30 days to investigate and respond to your dispute. Regularly check the status of your dispute, and follow up promptly if there are any delays or if additional information is requested.

In case the credit bureaus failed to reply after 30 days, do this.

Additional Actions For Unauthorize Hard Inquiries

If you discover unauthorized hard inquiries on your credit report, it’s essential to take additional actions to address the situation.

Place a fraud alert on your credit reports. This adds an extra layer of protection by requiring creditors to verify your identity before extending new credit. You can place a fraud alert with one of the credit bureaus, and they will notify the others.

If you believe you are a victim of identity theft, file a report with your local police department and obtain a copy of the report. You can use this identity theft report to support your dispute with the credit bureaus.

Reach out to the creditor associated with the unauthorized inquiry. Explain the situation and ask for details about the inquiry. In some cases, the creditor may provide information. Or if the inquiry was made in error, they may be able to remove the inaccurate hard inquiry within 24 hours.

If necessary, you can extend the fraud alert beyond the initial 90-day period. Then, consider a credit freeze for added protection.

Step 4: Use Rapid Rescore Services

One of the fastest ways to remove inaccurate inquiries is using a Rapid Rescore Service. However, it’s important to note that this service is not directly available to individual consumers. They are offered by lenders or mortgage brokers when a borrower is in the process of securing a mortgage. So, if you want to remove hard inquiries quickly, ask your creditor if they have this program.

The primary purpose of Rapid Rescore is to expedite the correction of inaccuracies or updates on your credit report. Hence, to reflect recent financial behavior.

Step 5: Get Your Result

After you dispute an item on your credit report, the credit bureau will investigate. Once the investigation is complete, they will send you a written response by mail. This response will include the results of the investigation, like any changes made to your credit report.

While the process is primarily conducted through traditional mail, some credit bureaus may provide online dispute resolution tools where you can track the status of your dispute. These online platforms might send notifications or updates via email to inform you of the results of your dispute.

Is it Possible to Remove Hard Inquiries within 24 hours?

Removing hard inquiries from your credit report within 24 hours is unlikely and generally impossible. The credit agencies are required by law to conduct a thorough investigation within a reasonable time frame.

The Fair Credit Reporting Act (FCRA) mandates that credit bureaus must investigate disputes within 30 days of receiving them. While the investigation may be completed sooner, the 30-day window is the standard timeline.

Additionally, some disputes may take longer, especially if they require additional information or documentation.

Beware of services or claims that promise rapid removal of hard inquiries within extremely short timeframes. Because they may be misleading or even fraudulent. Legitimate credit repair processes adhere to the regulations set by the FCRA and focus on accuracy and fairness in credit reporting.

If you’re concerned about hard inquiries on your credit report, the recommended approach is the steps provided above. Be patient during this process, as resolving disputes takes time to ensure a thorough and accurate investigation.

How can the Credit Money Machine Help you remove Hard Inquiries?

Credit Money Machine has an automated credit dispute process. When you extract credit reports inside the software, it automatically detects errors. This includes discrepancies in inquiries, including unauthorized inquiries.

Moreover, the software ensures you won’t mistakenly dispute positive accounts to protect your credit score.

Here’s a video on how to easily pinpoint what inquiries to dispute with Credit Money Machine.

Automate the Process

Whether you want to remove hard inquiries in your credit reports or for your clients as a credit repair specialist, we have the right software for you.

15 seconds processing in just one click

Alternatively, you can Book a Live DEMO for free to see our powerful software in action.

For credit repair business start-ups, I recommend learning about credit repair laws to avoid legal issues and a guide on how to start credit repair business.